Individuals are imperfect and will continue to be prone to biases. The key to success in markets is to first acknowledge the existence of biases, and then put in place processes to manage biases, especially at exits.

China recently eased restrictions under the Zero Covid policy and is reportedly going through a large Covid-19 wave. This has started causing concerns amongst financial market participants, which highlights a very important aspect of investor behaviour. Investors often operate based on emotional biases than long-term fundamentals.

“There is always an element of over-reaction in the market to Covid-19 news,” stated a Chief Investment Strategist at one of the broking houses. Uncertain times cloud investors’ judgments, often triggering actions based on emotions. Such instances showcase that the Efficient Market Hypothesis doesn’t always hold and how investors’ biases ultimately influence their investment decisions. As stated by Morgan Housel, “Investing is not the study of finance. It’s the study of how people behave with money”.

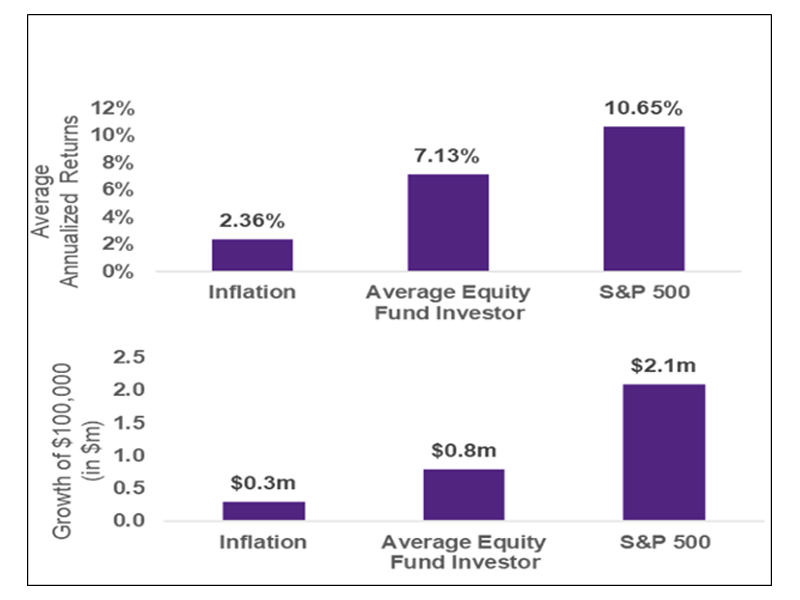

As per a study by Dalbar, a financial-services firm, equity fund investor returns stood at ~7.1 percent p.a. versus ~10.7 percent p.a. for broader market indices such as S&P 500. This difference is attributed to investor biases. Dalbar showcases why investors need to regulate emotions to earn higher returns.

The inability to regulate emotions/biases is termed a ‘Cognitive Error’. In the book ‘The Art of Thinking Clearly’, Rolf Dobelli defines Cognitive Errors as systematic deviations from logic and rational behaviour; barriers to logic that we stumble upon repeatedly. Over time, these deviations aggregate up towards broader market anomalies which lead to bubbles and crashes.

Behavioural Biases amongst finance experts

Mutual Funds and Hedge Funds

The mutual fund industry has grown over 28 times in the last 20 years and is expected to grow at a CAGR of ~22 percent soon. In our conversations, a Hedge Fund manager highlighted how financial experts are also prone to Cognitive Errors. For example, a hedge fund that takes corresponding long and short positions should ideally be transactional and unbiased. But in reality, greed can affect fund manager decisions, and fund managers end up holding on to positions even after meeting the returns thresholds.

The fund manager we spoke to opined that “The longer you are in the industry, the more likely you are to develop biases”. Especially, when a fund manager has had prior experience in a particular industry, he/she may develop a confirmation bias for assets belonging to that segment. Analysts may even notice a higher conversion rate for recommendations from that industry. So, a manager needs to build a team that is comfortable presenting opposing and concrete views. This prevents fund managers from falling prey to any preconceived judgments.

Trading

While mutual funds hold assets for a longer-term outlook, traders look for quick short-term wins, moving in and out of stocks within days or even minutes. However, trading and leveraged positions are highly vulnerable to Black Swan events. A trader’s biases can further complicate and lead to higher losses.

In our conversations with an energy and fixed-income derivatives trader, human biases primarily impact a trader’s exit positions. Fear, greed, or regret come into play during the exit. So traders try to minimise the effects of these factors through algorithms. These algorithms automate the entry, exits, and lot sizes. Thereby, it removes all elements of human emotions and mechanizes the entire process.

Traders also develop their decision-making algorithms called ‘black boxes’. These algorithms are exclusive to each trader. The trends and worst-case scenarios are back-tested to be integrated into the well-defined risk of their model. They also provide the flexibility to integrate certain tested biases into the software. However, the algorithms aren’t capable of reading or analysing the news and may need some manual intervention from time to time. Nonetheless, these models ensure that decisions are not made based on fear, regret, or greed. According to the trader we spoke to, “Clockwork-like discipline in your strategies despite the external circumstances is what makes you money in trading”.

After speaking to these experts, we reaffirm the view that individuals are imperfect and will continue to be prone to biases. The key to success in markets is to first acknowledge the existence of biases. Technical expertise alone is not sufficient. And then put in place processes to manage biases, especially at exits. External events such as Covid-19 will continue to test our biases. It is times of such crises that separate men from the boys; the investors with better investment processes from the novices and impulsive traders.

This article was originally published in Forbes India.

Link to the article: https://www.forbesindia.com/article/bharatiya-vidya-bhavan039s-spjimr/bringing-method-to-the-madness-a-hedge-fund-manager-and-derivative-traders-take-on-behavioural-biases/83033/1