India witnessed ~49bn real-time payment transactions, more than any other country in the world.[1] The credit for this feat goes to the National Payments Corporation of India (NPCI). NPCI is at the forefront of the Indian payment systems success story, with its flagship product UPI; Unified Payments Interface. UPI is an instant real-time payment system that enables peer-to-peer (P2P) and person-to-merchant (P2M) transactions.

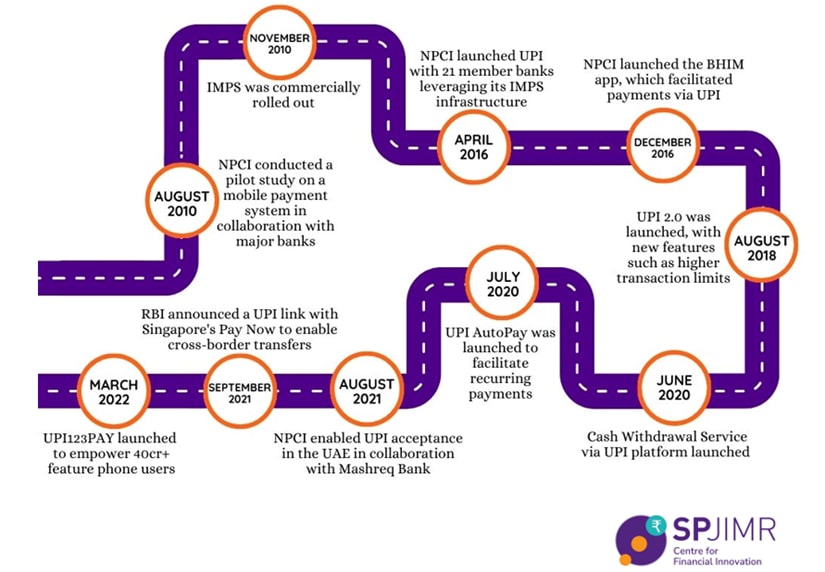

Figure 1: NPCI’s Journey  Source: Author’s Contributions

Source: Author’s Contributions

UPI: Present Scenario

The total value of the transactions via UPI has reached ~10.6 lakh crore and further, UPI is taking a lion’s share of other payment platforms such as NEFT.[2] Further NIPL (NPCI International Payments Limited), the wholly owned subsidiary of NPCI is now focussing on taking UPI international. NIPL has facilitated cross-border transactions via UPI and is present in 10+ countries with its latest venture into the European Market. Partnership with UK-based PayXpert will facilitate the Rupay and UPI network to integrate beyond the Asian space.

Figure 2: Value of UPI Transactions  Source: Reserve Bank of India

Source: Reserve Bank of India

Challenges

UPI has still deemed an urban success story. According to research by 1Bridge, a social tech enterprise operating in the village commerce network in India, only 3-7% of rural customers are actively using UPI to transact. Around 40% of those surveyed were unaware of UPI and digital payments.[3] Further, the long-term financial viability of UPI is a concern for banks and NPCI. UPI is a free service provided by NPCI, resulting in significant operational losses. Further, UPI will need constant investment in technology infrastructure. The entire IT infrastructure of NPCI demands best-in-class technology and maintenance. This, in itself, is a mammoth expense that will grow further in the future. Now given UPI’s large share in payments, the financial viability of UPI is important for financial stability.

As per a recent discussion paper by the RBI, the stakeholders collectively incur ~ ₹ 2 for

As per a recent discussion paper by the RBI, the stakeholders collectively incur ~ ₹ 2 for processing a UPI-P2M transaction with an avg. transaction value ~ ₹ 800. This translates to a total of 0.25% of the total transaction.[4] While this appears to be very small and attractive compared to the MDR rates applicable to other modes of digital payments, one must note that the entire cost is borne by the govt. in terms of incentives. As of 2022, the subsidy provided by the govt. was @ ₹ 1,300 crores. Considering the rising volume of transactions taking place, this subsidy won’t suffice to maintain and upgrade the required infrastructure. A widening gap can add to the existing woes of increasing downtime in the UPI service.

While the govt. spends almost ₹ 5,000 crores for maintaining the physical currency in circulation, a transition was definitely called for. However, if we see the recent trends in usage, the explosive adoption patterns suggest a 100% growth rate in UPI volume and 75% growth in its value for the past 1 year.

Currently, India has around 30 crores of unique UPI users and the move of linking credit cards to the UPI method is yet another challenge. If one talks of growth in UPI adoption, we are far from reaching saturation levels. Compared to the smartphone penetration rate of ~45.7% in India, much less than 50% of smartphone users are using UPI. As of 2021, the share of UPI among all payment methods accounted for ~31.3% which is expected to grow up to ~70.7% by 2026. This number should not be assumed at the present level of transactions as India is headed for healthy growth and an ambitious $5 trillion GDP economy by 2025.

The entire scenario is slated considering the domestic scenario at the place. If one considers the growth in MOUs and partnerships with other economies, there is a high need for massive levels of investments in the infrastructure for the India Stack.

Possible Solutions

As of December 2022, 382 banks are live on the UPI Platform generating INR 12.8 lakh crores of value and 782 crores of transaction volumes with an average ticket size of INR 1,640 per transaction.[5] So, the question is in what ways can UPI be monetized to meet the operational costs of the platform?

Option 1: Levying a transaction fee beyond a certain minimum limit of payments. This will ensure payments by retail and MSMEs users are not affected and we continue to pursue the drive towards a cashless economy. However, this move does not seem to be very effective if we consider the case of ATM withdrawals as an example. Charges on withdrawal after a certain number of transactions per month highly discouraged the users to use the ATM and forced them to either change their ATM usage habit or shift to alternate modes. Fintech Apps like PhonePe and Paytm also faced a sharp decline when they started charging convenience fees for electricity bill payments and wallet top-ups via credit card respectively.

Option 2: Make UPI a subscription-based product where the users will have to pay a nominal fee and the user will be able to use the UPI platform freely. A nominal fee will ensure the elimination of inefficient users. Though subscription-based Fintech products are not a common picture. Many of the Fintech players in the market are yet worried. For a rough comparison, only 119mn out of 424mn OTT users in India are active paid subscribers.[6] Though these numbers might not show the actual trend due to multiple factors including different industries, one can be very well derived from a price-sensitive market like India where growth with a subscription cost will slow things down initially but will grow in the long run.

Option 3: This option is the amalgamated result of the above two options where the UPI platform can be used as a freemium product. The basic services of UPI to transfer money can be used freely and above a certain threshold, users need to pay a premium for the benefits of high-volume transactions. This seems to be feasible as it neither hurts P2P nor P2M users for simple day-to-day low-denominated transactions. This will ensure constant R&D and development in infrastructure. It will also enable non-govt. entities to widely adopt UPI without finding alternate ways of revenue streams such as commissions on utilities, risk of data leakages etc. To take an example, out of Moneycontrol’s ~ 40mn+ monthly unique users, only ~0.5mn users are their premium (Moneycontrol Pro) users as of May 2022.[7] This shows a high willingness for user adoption and a revenue-generating user base for advanced features.

As Ramesh Narasimhan, the CEO of Worldline India quotes, “UPI is now a juggernaut in its own right. It’s a train that has left the station”,[8] NPCI has a serious responsibility to shoulder in balancing the sustainability and growth of a faster and integrated payment system.

References:

1. https://www.livemint.com/news/india/40-of-global-real-time-payments-originated-in-india-in-2021-report-11650973119569.html

2. https://www.fortuneindia.com/macro/july-upi-transaction-value-hits-all-time-high-at-106-lakh-cr/109176

3. https://timesofindia.indiatimes.com/blogs/voices/ecommerce-penetration-in-rural-india-challenges-barriers-and-solutions/

4. https://www.rbi.org.in/Scripts/PublicationsView.aspx?id=21082

5. https://www.npci.org.in/what-we-do/upi/product-statistics

6. https://www.livemint.com/industry/media/india-has-424-mn-ott-viewers-119-mn-paid-subscriptions-report-11670393943769.html

7. https://www.moneycontrol.com/news/business/moneycontrol-pro-rises-to-no-14-in-the-top-20-global-digital-news-subscription-services-8483321.html

8. https://www.business-standard.com/shows/banking-show/worldline-india-ceo-ramesh-narasimhan-talks-about-upi-and-more-2359.htm